Kathrin Glau joined the School of Mathematical Sciences, Queen Mary Universtiy of London as Lecturer in Financial Mathematics in September 2017. During the academic year 2018-2019 she was a Fellow at the Swiss Finance Institute at the Ecole Polytechnique Fédérale de Lausanne. From 2011 to 2017 she was Assistant Professor (Juniorprofessorin)

at the Department of Mathematics, Technical University of Munich. Prior to this

she completed her Ph.D. on the topic of

Feynman-Kac representations for option pricing in Lévy models in 2010

(supervisor Ernst Eberlein) and moved to the University of Vienna to work as a university assistant at the chair of Prof. Walter Schachermayer.

News

New Investigator Award for the research project Deep Learning Reduced Basis Method for High-Dimensional Parametric Partial Differential Equations in Finance

offered by the EPSRC

Awards

DERI Fellow 2021 - present

Turing Fellow: Fellow at the Alan Turing Institute 2018 - 2021

EPFL FELLOW co-funded by Marie Skłodowska Curie 2018 - 2019

TUM Junior Fellow 2011-2017

Interactive art project creating the mathematical universe at TateExchange, Tate Modern, London

Thank you all for joining us in creating the mathematical universe at TateExchange, June 11-16 2019!

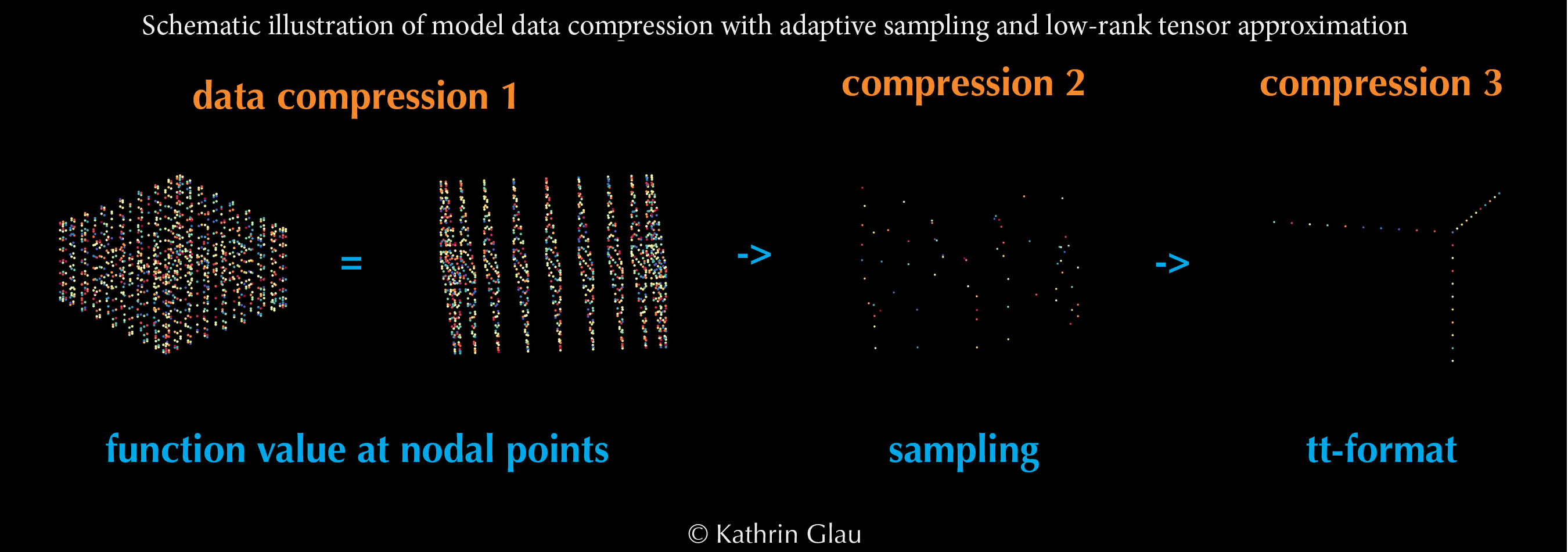

Computational methods for finance and beyond (Fourier, P(I)DE, complexity reduction, interpolation), Modelling of financial asset evolution (with Lévy and other jump processes)

Glau, K.; Grbac, Z.; Papapantoleon, A.:A Unified View on LIBOR Models.

In J. Kallsen, A. Papapantoleon (Eds.), Advanced Modelling in Mathematical Finance -- In Honour of Ernst Eberlein, pp. 423-452, Springer, 2016

preprint available on arXiv: 1601.01352

Eberlein, E.; Glau, K.; Papapantoleon, A.: Analyticity of the Wiener-Hopf Factors and Valuation of Exotic Options in Lévy Models. Advanced Mathematical Methods for Finance, 2011, 223-245

preprint available on arXiv: 0911.0373

2010

Eberlein, E.; Glau, K.; Papapantoleon, A.: Analysis of Fourier Transform Valuation Formulas and Applications. Applied Mathematical Finance (17/3), 2010, 211-240

preprint available on arXiv: 0809.3405